Featured

Table of Contents

Browsing Credit Recovery in Jacksonville Debt Relief

The financial environment of 2026 has actually presented distinct pressures on home budget plans, leading lots of individuals to consider insolvency as a path toward monetary stability. Declare insolvency stays a significant legal choice with lasting implications for credit rating. While the immediate impact is typically a sharp drop in point overalls, the trajectory of a score in the years following a filing depends heavily on the kind of personal bankruptcy picked and the subsequent actions taken by the debtor. In 2026, credit report designs continue to weigh public records heavily, however they likewise place increasing importance on recent payment history and credit utilization ratios throughout the recovery stage.

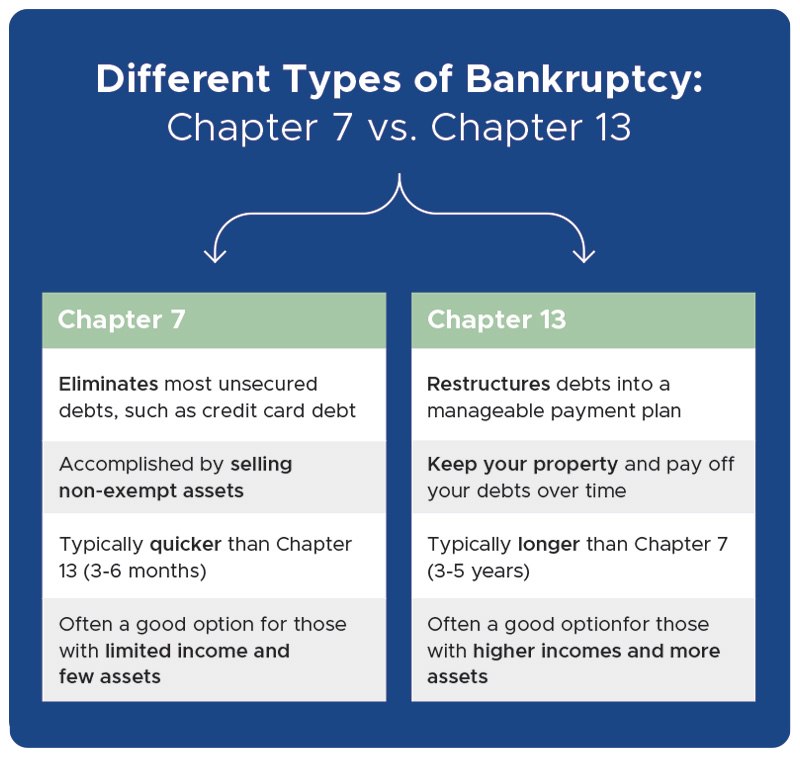

For those residing in the surrounding region, comprehending the difference between Chapter 7 and Chapter 13 is the initial step in handling long-lasting expectations. A Chapter 7 filing, which includes the liquidation of non-exempt properties to release unsecured financial obligations, remains on a credit report for ten years from the filing date. In contrast, Chapter 13 involves a court-mandated 3 to five-year payment strategy and stays on the report for seven years. Numerous homeowners in Jacksonville Debt Relief begin their recovery by checking out Debt Management to better comprehend their legal standing before proceeding with a filing.

The Role of Nonprofit Credit Therapy in 2026

Navigating the complexities of the U.S. Bankruptcy Code in 2026 needs more than just legal documents. U.S. Department of Justice-approved 501(c)(3) not-for-profit credit therapy firms have become a main resource for those looking for a method out of financial obligation without necessarily turning to the courts. These organizations, such as APFSC, provide necessary pre-bankruptcy therapy and pre-discharge debtor education, which are legal requirements for anybody pursuing a bankruptcy discharge. These services ensure that people in the United States are totally mindful of their alternatives, consisting of financial obligation management programs that may function as an option to insolvency.

A debt management program (DMP) operates in a different way than a legal discharge. In a DMP, the agency deals with financial institutions to consolidate month-to-month payments into a single, more workable amount. These programs frequently result in lowered interest rates, which can be more useful for a credit score over time than a bankruptcy filing. Comprehensive Debt Management Programs stays a typical service for those having problem with high interest rates who wish to prevent the ten-year reporting period connected with Chapter 7. By selecting this path, customers in the broader community can frequently preserve their credit standing while systematically eliminating their financial obligation load.

Credit Rating Characteristics Post-Bankruptcy Filing

Right away after a personal bankruptcy is discharged in 2026, the credit score usually hits its lowest point. The impact reduces as the filing ages. Scoring algorithms are designed to favor current behavior over historical errors. This indicates that constant, on-time payments on new or remaining accounts can begin to pull a score up even while the bankruptcy remains noticeable on the report. For numerous in Jacksonville Debt Relief, the key to a quicker healing lies in monetary literacy and the disciplined use of protected charge card or credit-builder loans.

Not-for-profit agencies like APFSC likewise offer HUD-approved real estate therapy, which is particularly relevant for those worried about their ability to lease or purchase a home after an insolvency. In 2026, loan providers still look at personal bankruptcy filings, however they are often more lenient if the candidate can show a number of years of clean credit report post-discharge. Consulting with professionals regarding Debt Management in Jacksonville helps clarify the differences between liquidation and reorganization, allowing individuals to choose that line up with their long-term real estate objectives.

Handling Debt through Strategic Collaborations

The reach of credit counseling in 2026 has broadened through co-branded partner programs and networks of independent affiliates. These partnerships permit organizations to offer geo-specific services across all 50 states, guaranteeing that someone in the local region has access to the exact same quality of education and support as somebody in a significant urbane location. These firms work closely with banks and community groups to offer a security net for those dealing with foreclosure or frustrating charge card balances.

Education is a core part of the services supplied by 501(c)(3) nonprofits. Beyond the legal requirements for bankruptcy, these agencies concentrate on long-term financial health. They teach budgeting skills, savings strategies, and the subtleties of how credit mix and length of history impact the modern-day 2026 scoring designs. For a person who has just recently gone through a personal bankruptcy, this education is the distinction in between falling back into old patterns and maintaining a stable climb towards a 700-plus credit rating.

Long-Term Healing and Financial Literacy

By the time a bankruptcy reaches its third or 4th year on a credit report in 2026, its "sting" has substantially decreased if the individual has actually remained debt-free and made every payment on time. The legal debt relief offered by the court system provides a clean slate, however the not-for-profit sector provides the tools to handle that start successfully. Agencies operating nationwide guarantee that financial literacy is available to diverse neighborhoods, assisting to bridge the space between insolvency and monetary self-reliance.

A single lower monthly payment through a financial obligation management program is often the very first step for those who are not yet ready for insolvency. By working out directly with creditors, these programs assist customers stay present on their obligations while decreasing the overall expense of the financial obligation. This proactive technique is extremely related to by lenders in Jacksonville Debt Relief, as it demonstrates a dedication to payment that a bankruptcy filing does not. Whether a specific picks a legal filing or a structured management plan, the goal in 2026 remains the exact same: accomplishing a sustainable monetary future where credit scores ultimately reflect stability rather than past difficulty.

The course to 2026 credit health after insolvency is not a fast one, however it is predictable. With the assistance of HUD-approved counselors and DOJ-approved education providers, the complexities of financial obligation relief become manageable. Each state and local community has actually resources devoted to assisting citizens comprehend their rights and responsibilities. By using these services, consumers can browse the legal system and the credit reporting market with the knowledge necessary to reconstruct their lives and their scores.

{kind=link}

Latest Posts

Analyzing Modern Debt Relief Alternatives

2026 Analyses of Credit Counseling Programs

Preparing for Financial Stability in the Coming Year